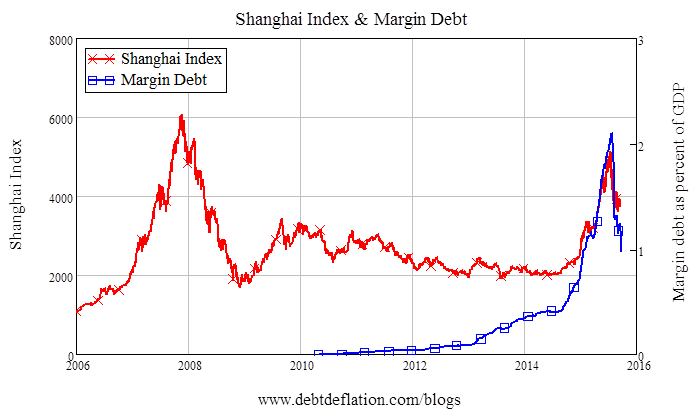

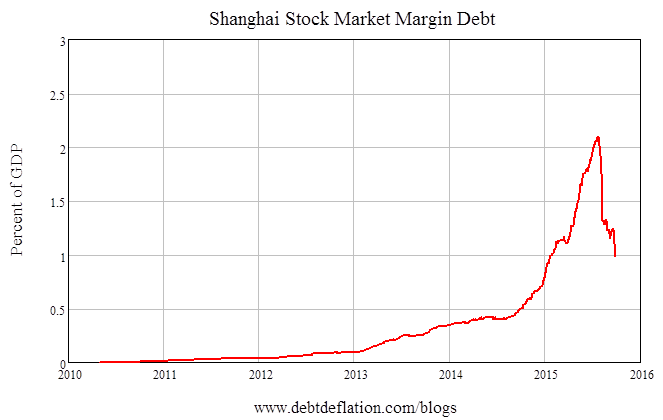

One thing my 28 years as a card-carrying economist have taught me is that conventional economic theory is the best guide to what is likely to happen in the economy. Read whatever it advises or predicts, and then advise or expect the opposite. You (almost) can’t go wrong. Nowhere is this more obvious than in its strident assurances that the value of shares is unaffected by the level of debt taken on, either by the firms themselves or by the speculators who have purchased them. This theory, known as the “Modigliani-Miller theorem”, asserted that since a debt-free company could be purchased by a highly levered speculator, or a debt-laden company could be purchased by a debt-free speculator, therefore (under the usual host of Neoclassical “simplifying assumptions”, which are better described as fantasies) the level of leverage of neither firm nor speculator had any impact on a firm’s value—and hence its share price. The sole determinant of the share price, it argued, was the rationally discounted value of the firm’s expected future cash flows. Armed with that theorem, I was always confident of the contrary assertion: that debt played a crucial role in determining stock prices. So, like the fictional 19th century French detective who began every investigation with the cry “Cherchez La Femme!”, my first port of call in understanding any stock market bubble is “Cherchez La Debt!”. It took a while to locate Shanghai’s margin debt data (the easier to find stock index data is here), but once I plotted it, the reliability of my trusty old contrarian indicator was obvious. While these figures may well substantially understate the actual level of margin debt [see also here], they imply that, starting at the truly negligible level of 0.000014% of China’s GDP in early 2010, margin debt rose to over 2% of China’s GDP at its peak in June of this year. It has since plunged to just under 1% of GDP—see Figure 1. Figure 1: Margin debt as a percent of China’s GDP: from 0.000014% to 2% in 5 years–and back down again image002 The ups and downs of margin debt have both paralleled and driven the stock market boom and bust in China: as the leverage of speculators rose and fell, so did the market—see Figure 2. Figure 2: A debt bubble begets a stock market bubble image004 This isn’t just correlation. As I explained briefly here, demand in our economies is the sum of demand from the turnover of existing money, plus demand from newly created money—which overwhelmingly comes from bank lending. This demand is then spend on both goods and services, and assets—property and shares. Since leverage forms a large part of the demand for property (via mortgages) and shares (via margin debt, and the leverage used by professional stock market firms to amplify relatively small gains from high frequency trading and the like), the flow of demand into these markets is largely determined by the change in the relevant type of debt. The flow of supply is the flow of existing or new assets being placed onto the market for sale, and is much less volatile than demand. If the two flows are roughly equal, then the price index will remain constant. There is thus a causal link between the rate of change of margin debt and the level of stock prices (and ditto a link between the rate of change of mortgage debt and the level of house prices). This implies a causal link between the acceleration of margin debt and the change in stock prices—which is borne out for China by Figure 3. Figure 3: The correlation between margin debt acceleration & monthly change in the Shanghai index is 0.69 since 2014 & 0.87 since 2015 image006 Just as the Chinese private sector dived into debt far faster than America or Japan, Chinese speculators have dived into margin debt far faster than their Yankee counterparts. It took America 9 years to go from margin debt being 0.5% of GDP to 2%; China made that transition in about 10 months (see Figure 4). They are piling out just as quickly, and the end of that process is nowhere near in sight. Figure 4: Chinese margin debt has risen much faster than the USA’s

Source: Why China had to crash: Part 2 | Real-World Economics Review Blog